The essential insights you need to plan for peaks and get ahead in 2024

Rob Gill &

Rob Gill &  Tom Parry

Tom ParryWith the always-anticipated peaks period just around the corner – but economic constraints and geopolitical uncertainty aplenty – how are consumers and industry chiefs feeling about 2024? In association with PwC, TTG’s latest Agenda 2023 report explores the trends, challenges and opportunities for the trade in the year ahead...

Holidays will continue to be a priority spending area for UK consumers in 2024, with many opting to cut back in other areas to “protect” their overseas trips.

The latest survey of 2,000 consumers by PwC found continued “strong demand for holidays”, reflecting many of the trends seen in previous surveys throughout this year. Most people (around 70%) plan to spend the same or more on holidays next year as they did in 2023, with only 15% likely to cut holiday expenditure.

Eleanor Scott, partner at Strategy&, part of the PwC network, assesses: “On balance, people expect to spend more on holidays in 2024 than they did this year, particularly among higher income and older age groups. This is partly due to high holiday costs but also as people plan to take more holidays or longer/more premium options.”

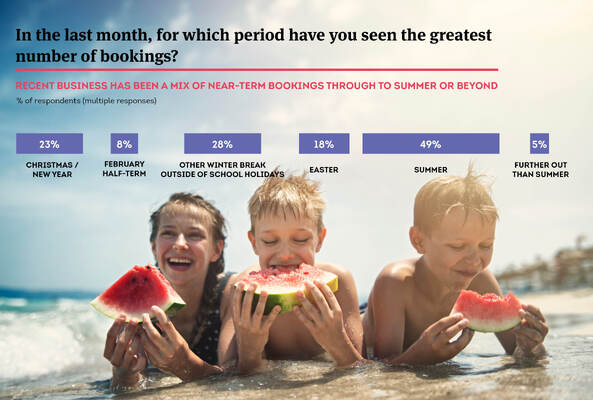

POLARISED BOOKING HABITS

Plenty of headwinds remain, however, with the biggest barriers to travel being the rise in holiday prices (32%) and concern over household finances (22%), despite the recent easing in overall inflation.

“This could impact what types of holidays people take and cause them to wait to see what they can afford before booking – leading to a late booking profile for some market segments,” adds Scott.

The survey reflects the “polarisation” in consumer buying habits with this year’s trend of strong early and late bookings set to continue in 2024. There’s plenty of indecision in the market, too, with 17% currently not planning to go on holiday next year and 19% yet to decide on potential destinations.

“Consumers are still very positive but they are more unsure about whether they’ll go and if so, where they’ll go. Whether confidence was bolstered a bit this time last year because there was still that pent-up demand, now you’ve had a prolonged period of pressures on households and you’ve reached a point of more uncertainty.”

MARKETING MESSAGE SHIFT

Quizzed in the research for their reasons behind waiting to book, consumers described being increasingly price conscious in their mindset.

Asked to select up to three marketing messages that best resonated to make them both with a travel company, consumers choices of “value” (41%), “special offers” (33%) and “low deposit/buy now pay later” (14%) made up three of the four most popular options.

“Last year it was a lot more about inspiration but this year it’s value-led,” added Scott.

While Europe and the UK remain the top choices for consumers, they have both declined in popularity year-on-year. Conversely, there has been an increase in demand for long-haul options such as Asia and Australasia.

Travel firms are expecting to achieve higher revenues and profits in 2024 than this year but challenges remain for the sector, including the state of consumers’ finances and the impact of conflicts on travel.

A survey of more than 40 travel companies by PwC found a mood of “cautious optimism”, with growth being a top priority for 64% of firms – up by 15 percentage points on autumn 2022’s poll.

Scott says: “Travel leaders are optimistic over the outlook for 2024, with most expecting increased revenues and profits relative to 2023.

“It’s obviously early days in terms of bookings for next year but a number of respondents commented that bookings are up at this point or expect them to go up as consumer pressures ease.”

Continued conflict disruption?

But the potential impact on travel from geopolitical events, such as the ongoing war between Israel and Hamas, has shot into the list of the top barriers to growth – 46% of firms said that conflicts could impact their sales in 2024.

While industry bosses’ worries over recruitment and retention have fallen sharply compared to previous surveys, concerns over cash flow requirements has made an unwelcome return.

“I do wonder if there’s a bit of stress coming into the system,” assesses Scott. “That could be paying off suppliers, paying off interest from Covid-accumulated debt… [cash flow requirements] hasn’t been as much of an issue since the early periods of Covid.”

Scott says travel firms will “require agility to successfully navigate” any impact from conflicts, as well as extreme weather and other types of disruption in 2024.

“Companies are going to have to be adaptable. Firms are focusing on building resilience and cost management as well as positioning for growth over the coming year,” she adds.

Twin Peaks?

As the post-Christmas peaks period rapidly approaches, most firms expect to spend at least the same or more on marketing than last year, although there were mixed views on the timing of campaigns.

“We could potentially have two peak booking periods next year given the polarisation in booking timings we saw this year and the indications consumers have given us on when they expect to book,” says Scott.

“My takeaway is you’re going to have to be very flexible and pull back quickly if there isn’t the demand there to justify that spending. Particularly if you’re going to have a late peaks period, then you’re going to need some of your war chest saved for then.”

Read PwC’s full consumer and trade research in our latest Agenda 2023 Winter report

Sign up for weekday travel news and analysis straight to your inbox

Tom Parry

Rob Gill

Supplier Directory

Find contacts for 260+ travel suppliers. Type name, company or destination.

Recommended For You

Competitions

TTG Luxury Journey

Place of registration: England and Wales.

Company number 08723341.

Registered address: 6th Floor, 2 London Wall Place, London EC2Y 5AU